U.S. State Payday Lending Regulations

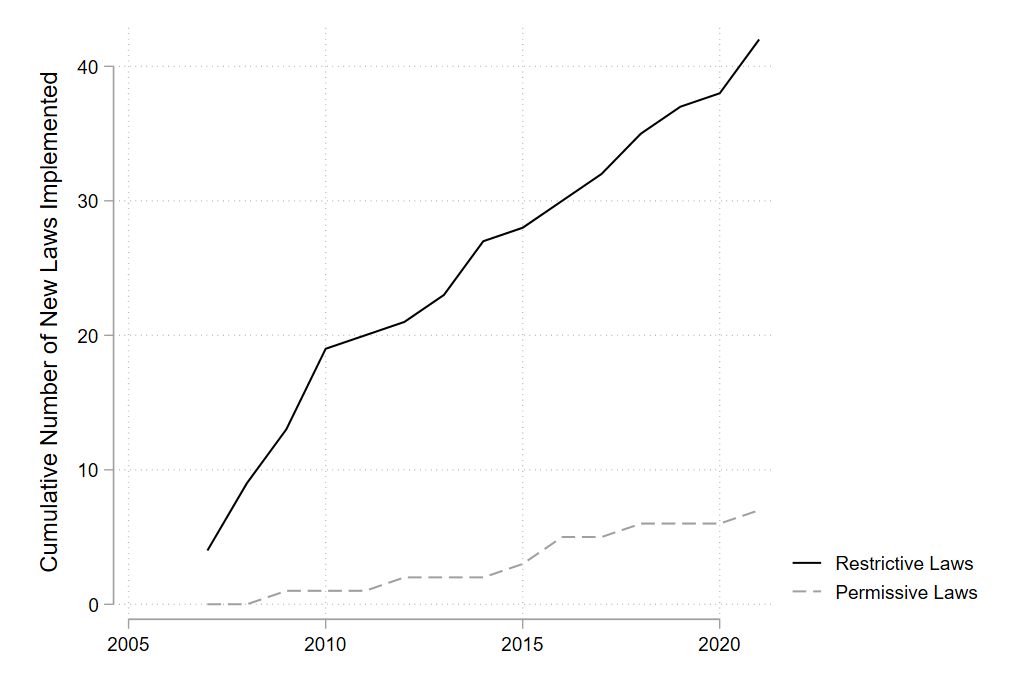

Payday lending provides access to short-term small-dollar loans but at significant cost to borrowers and reinforces inequalities in U.S. financial markets. States have authority to regulate these loans above and beyond federal regulation, although questions remain about their effectiveness. We introduce a state payday lending regulation database that we link to proprietary data on the availability and use of high-cost credit. We estimate two-way fixed effects models that predict changes in payday lender and borrower behavior as states strengthen or weaken regulations. We find that as regulations grow more restrictive, the supply and use of payday loans decline, particularly for low-income and non-white populations. Restrictions that target the cost and time dimensions of payday lending are more strongly associated with supply and loan use reductions than policies that target lender compliance. Our findings can inform policy debates over ways to better protect American consumers and reduce inequalities in financial markets.

with Megan Doherty Bea, Victoria Coan, and Rachel E. Dwyer